The real reason Trump's tax bill is 'historic'

Trump has single-handedly shoved the United States to the brink of economic calamity

At Donald Trump’s urging, the U.S. House has narrowly passed a tax bill that he describes as “arguably the most significant piece of Legislation that will ever be signed in the History of our Country.” If Trump turns out to be right, it won’t be because the bill inaugurates the “golden era” of economic growth he has been promising. If the Senate abandons every last pretense of fiscal sanity and sends the bill to Trump’s desk, this will drastically raise the risk of a U.S. debt crisis that could send the entire global economy into turmoil. In less than five months, Trump has single-handedly thrown the United States’ historic role as the anchor of the global financial system into doubt. The real scandal isn’t that Trump is fixated on self-destructive economic policies like tariffs and tax bills destined to become debt bombs—it’s that Congress has allowed him to put the economy in peril without a squeak of opposition.

On May 16, Moody’s downgraded the United States’ credit rating from Aaa to Aa1. The agency cited the failure to “agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs. We do not believe that material multi-year reductions in mandatory spending and deficits will result from current fiscal proposals under consideration.” This is a significant understatement. The Congressional Budget Office (CBO) reports that the tax bill will cost $3.8 trillion over the next decade. However, the Committee for a Responsible Federal Budget predicts that the bill will add $5.3 trillion to deficits if its “expiring policies are extended permanently.” These eye-watering numbers will be counteracted by $1.3 trillion in cuts to programs like Medicaid and food stamps, which the Senate is likely to reduce.

Trump has never been forced to confront fiscal realities like he faces now. When he passed his deficit-ballooning 2017 tax cuts, the average interest rate was less than 2.3 percent. Even amid a flurry of COVID spending in 2020, interest rates remained low and the cost of debt service was manageable. Then came the post-COVID inflation, which led to soaring interest rates and a much more onerous debt burden—in 2024, the U.S. government spent more on interest than national defense. Trump is unfazed by this dramatic change in the United States’ fiscal circumstances, which has led him to destabilize the global trading system with erratic tariffs that defy basic economic logic and push for the most irresponsible and regressive tax bill in modern American history. Meanwhile, Trump has been loudly demanding a reduction in interest rates and threatening to fire Fed Chair Jerome Powell—another move that roiled markets and sapped global confidence in the United States.1

Cynicism and short-term thinking are core features of populist politics—Trump tells Americans what he believes they want to hear and prioritizes political expediency over all other considerations. When entitlement reform became an important campaign issue during the 2015 GOP primary, Trump saw an opportunity to flex his populism: “Every Republican wants to do a big number on Social Security, they want to do it on Medicare, they want to do it on Medicaid,” he said at an event in New Hampshire. “And we can’t do that. And it’s not fair to the people that have been paying in for years.” Many Americans were attracted to a Republican presidential candidate who sounded like he wanted to boost the working class and defend the social safety net. Trump has repeatedly promised not to cut entitlements over the years, and the White House recently released this “fact check” on the subject: “The Trump Administration will not cut Social Security, Medicare, or Medicaid benefits. President Trump himself has said it (over and over and over again).”

The CBO estimates that Trump’s “BIG, BEAUTIFUL BILL” will cause 10.3 million people to lose their Medicaid coverage. Of course, there’s an easy way around an inconvenient fact like this—Trump can just lie. Yet again, he recently declared that “we’re not cutting Medicaid” and said the only people who will be thrown off the program are undocumented immigrants. This is not true.

Despite Trump’s naked hypocrisy, opportunism, and dishonesty, he has positioned himself as a friend of the working class with a message of economic populism—a message that has been consistent since his first term. “The forgotten men and women of our country,” Trump declared in his first inaugural address, “will be forgotten no longer.” Trump declared that American workers had been betrayed by elites who supported globalization: “For many decades, we’ve enriched foreign industry at the expense of American industry … We’ve made other countries rich while the wealth, strength, and confidence of our country has disappeared over the horizon.”

Trump said the “wealth of our middle class has been ripped from their homes and then redistributed across the entire world,” but as I observed a couple of weeks ago, per capita GDP in the United States has outpaced the UK, EU, Japan, and China for decades. Despite the tremendous benefits of the “exorbitant privilege” of printing the world’s main reserve currency—from lower borrowing costs which have historically funded disproportionate American growth to the ability to use the global financial system as a weapon against adversaries—Trump believes this privilege has been a curse. This has led his administration to repeatedly threaten to blow up the global economy and financial system with devastating tariffs and potentially catastrophic economic experiments like the “Mar-a-Lago Accord”—an effort to devalue the dollar while retaining its reserve status.2 Trump and some of his top economic advisors believe this can be done with various forms of coercion—such as threatening to impose tariffs or withdraw U.S. security guarantees—to bully other countries into accepting a cheaper American dollar while ensuring that the dollar remains at the heart of the global financial system. This is a reckless gamble, and it’s more likely to destroy confidence in the United States’ economic stewardship than to realize Trump’s stated goal of making American exports more competitive.

Trump’s commitment to protectionism is one of the few political positions he has consistently held over the decades—during a 1990 interview with Playboy, he said the United States’ allies and trading partners “walk all over us” and explained what he would do as president: “I’d throw a tax on every Mercedes-Benz rolling into this country and on all Japanese products.”3 Today, Trump touts what he calls an “external revenue service” to generate income for the U.S. government instead of taxes. But when the bond market thought Trump was actually committed to tariffs for the long haul, an alarming sell-off of U.S. debt promptly scared him into backing off—he drastically reduced his “liberation day” tariffs for a period of 90 days. This cycle has now been repeated so many times that Trump’s trade war threats have become hollow. When Trump recently declared that he would “recommend” a 50 percent tariff on the EU, he retreated within two days. Before Trump walked back the Europe tariffs, the S&P 500 dropped modestly—but it was clear that investors didn’t expect such a massive tariff to be imposed or to remain in place for long.

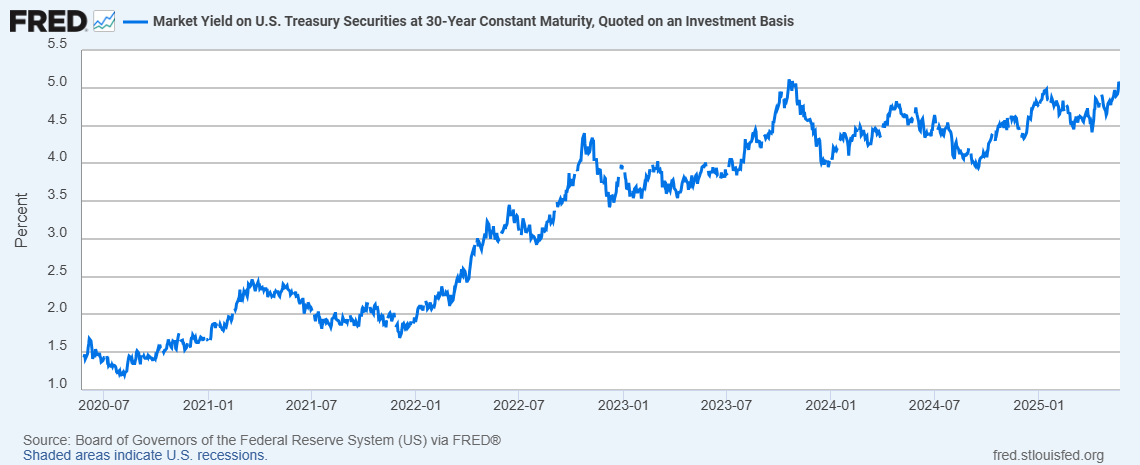

While the stock market has largely recovered from the “liberation day” shock, the 30-year Treasury yield is near its highest level since 2007.4 A recent U.S. Treasury auction revealed weak demand for American debt, and the dollar is continuing to founder as higher yields aren’t enough to attract new inflows of capital. As yields continue to climb, America’s fiscal picture looks even more unstable due to the growing proportion of the budget that must be allocated to servicing the debt. There are several catalysts that could cause investors to dump even more U.S. bonds: Trump signing the tax bill, the reimposition of tariffs, and selling by major foreign creditors like China and Japan. As Japan faces its own fiscal woes and its long-term yields hit multi-decade highs, this is a problem for the United States. Japan is the largest foreign holder of U.S. debt, and Japanese investors may be tempted to shift their focus to domestic bonds as those yields become more tempting. While Japan’s holdings of U.S. debt have increased in recent months, China (the United States’ third-largest foreign creditor) is selling.

The economist Paul Krugman recently published a sobering article about the possibility of what he calls a “sudden stop,” defined as an “abrupt cutoff of inflows of foreign capital.” While the United States has been able to sustain large deficits because the world has historically been eager to invest in American assets, Krugman points out that there’s no guarantee this will continue indefinitely. Although investors have so far been backing away from the United States at a steady pace (a process that appears stable for the time being), Krugman cites the economist Rudiger Dornbusch who argued that a financial crisis can take a “much longer time coming than you think, and then it happens much faster than you would have thought.” In the United States, the nightmare scenario would be a bond selling frenzy that would spark a vicious cycle: the government would be forced to borrow more to pay its existing obligations, which would worsen its fiscal position and drive even more selling.

Republicans pretend that the tax bill will create such a dramatic economic boom that growth will accelerate to a point where deficits will remain manageable. But this is extremely dangerous wishful thinking—Trump’s chaotic tariffs and other disastrous economic policies have decreased growth projections and increased the probability of recession. One potential outcome is that a debt crisis could trigger stagflation, which would leave the Fed with few tools to arrest the United States’ slide deeper into the financial abyss. This would lead to painful austerity measures at a time when Americans would already confront higher unemployment and prices.

While this scenario is by no means inevitable, the Trump administration and Republicans in Congress are willing to risk it. But for what, exactly? Trump has still failed to articulate a consistent rationale for his tariffs, which he sometimes presents as short-term negotiating tools and other times heralds as a long-term panacea that will fix the budget, create millions of manufacturing jobs (even though many of these jobs have been permanently lost to automation), and drive economic growth. Although the Court of International Trade recently struck down Trump’s tariffs, a federal appeals court reinstated them on Thursday. As Trump’s trade authority is battled out in the courts, his big, beautiful tax bill will snatch health insurance and food assistance for low-income Americans in exchange for a huge tax giveaway to the wealthy. In what may turn out to be this administration’s let-them-eat-cake moment, Treasury Secretary Scott Bessent recently said, “Access to cheap goods is not the essence of the American dream” and Trump declared that children will just have to get used to fewer toys as the country braces for his self-inflicted recession. Meanwhile, he’s preparing to take delivery of a luxury Boeing 747 from Qatar.

There’s only one explanation for the enactment of Trump’s dangerous, inconsistent, and almost certainly politically destructive economic policies—the Republican Party is now a cult of personality run by a capricious and incompetent authoritarian. Congress could retake the authority to impose tariffs from Trump at any time, but Republicans refuse to do so.5 Congress could have shown the world that the United States is still worthy of trust and investment, but Republicans refused to do so. Trump inherited a strong economy that had stabilized after years of global inflation,6 but he threw it away in a matter of months with the full support of his party.

The most distressing aspect of the Moody’s note about downgrading the United States’ credit rating wasn’t the agency’s observation that America is on an unsustainable fiscal path—it was the justification for the “stable” outlook America still has. Moody’s says this outlook “takes into account institutional features, including the constitutional separation of powers among the three branches of government that contributes to policy effectiveness over time and is relatively insensitive to events over a short period. While these institutional arrangements can be tested at times, we expect them to remain strong and resilient.” The world may soon discover that the strength and resilience of American democracy can no longer be taken for granted. At that point, the United States’ declining creditworthiness will be remembered as a symptom of a much deeper crisis.

Trump was wrong to demand cuts when interest rates were already extremely low before COVID, and he’s even more wrong now.

This plan was outlined in a November 2024 paper by Stephen Miran, the chair of Trump’s Council of Economic Advisers.

Japan was the big, scary rising Asian economy back then.

While the bond market stabilized after Trump walked back his EU tariffs, the delay is set to last until July. This isn’t going to stop, unless Congress finally grows a spine or Trump fails to defend his tariffs in the courts.

The Trump administration has justified the tariffs by invoking the International Emergency Economic Powers Act (IEEPA) of 1977, which gives the president the authority to unilaterally impose tariffs in the event of some “unusual and extraordinary threat”—such as war with a trading partner. The idea that the existence of trade deficits constitutes a “national emergency” is ridiculous, and the IEEPA declares that Congress can terminate this national emergency and restore its power to levy tariffs.

During the campaign, Trump insisted that the economy was in shambles and voters believed him. But unemployment was low, growth was strong, and the U.S. had managed to bring inflation down dramatically without causing a recession (the “soft landing” that many economists thought was impossible a few years ago).

Make America Great at Breadlines